We use cookies on Genome site to give you a better experience and to analyze and improve our

site

Cookies preferences

Genome uses cookies and other similar technologies to ensure stable operation of our site,

to monitor your performance on Genome site in order to improve its features, and to manage

our advertising campaign based on the interests of our audience.

By clicking ‘Accept all cookies’ you consent to the site using all necessary and

non-essential cookies.

If you want to modify cookie settings, click on ‘Manage cookies’.

We use cookies to provide Genome users with a smooth browsing experience. The data collected

by cookies is used to optimize Genome site for our visitors and deliver targeted information

to Genome users.

Necessary cookies allow the functionality of Genome site. They are always enabled. You can

disable the necessary cookies in your browser settings, but this may affect the accessibility

of Genome site.

Analytical and marketing cookies are used to improve Genome site and Genome services. For

analytical and marketing purposes we may use third-party technologies such as Hotjar,

Amplitude, Google Analytics and Google Ads. We may also advertise our services and products

on third-party websites, including social media, and use cookies of third parties on our

site to manage advertising campaigns.

To learn more about Genome and third-party cookies read our

Cookie Policy.

By checking the boxes below, you consent to install relevant cookies on your device. Genome

will not place any cookies on your device (except necessary) unless it’s allowed by you.

You can customize or disable cookies at any time following the instructions of our

Cookie Policy.

Genome Blog/articles/ The difference between a payment gateway, processor and a merchant account

Feb. 26, 2020

The difference between a payment gateway, processor and a merchant account

Online payments have already become an essential part of our daily lives. Some of us probably remember the transactions and payments years ago when we had to go somewhere to send the transfers or could pay only by cash at the store

And now, everything we need can be done in a minutes from our laptops and smartphones, heck, even watches! Have you ever thought which stages the money come through when you send or receive the payments online?

Not only for customers, but for the online merchants the processing of online payments can be intimidating as it seems like a labyrinth with lots of turns and players. And we understand your concern. Being an online merchant who accepts customers’ cards online, puts a lot of pressure on you in terms of security and processing of those transactions. That’s where the third-party companies come and cover these matters for you.

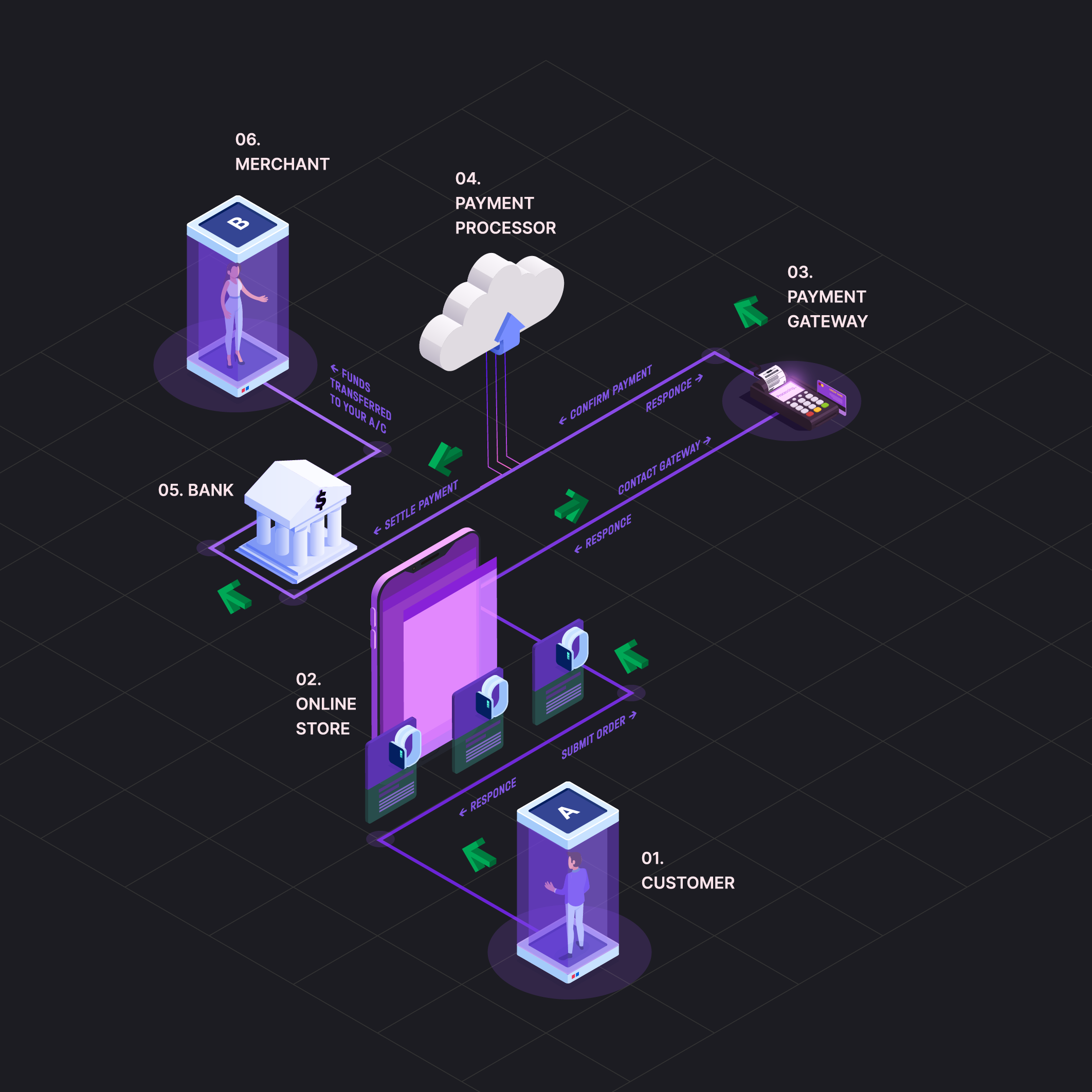

A person (customer) orders something (a product or a service) on a website, fills in the card information and presses confirm. Then he receives the confirmation about successful payment — the order was made.

From the other side the seller accepts the card payment on his merchant account after the verification of the transaction from the acquiring bank. All this happens in the matter of a minute.

So what are all these intermediaries are and what they do?

Payment Gateway

Payment Gateway — is one of key parties in the credit card transaction process.

PG is a tool/technology that processes card details and allows merchants to accept credit card payments. In online payments ecosystem, payment gateways usually use API’s (application programming interfaces) to collect card details from the merchant’s website when a customer makes an order. Simply put, the window we see on e-commerce websites, where we enter the details (number, expire date, CVV, etc) is a payment gateway. But why is this window (step) so important? It is a door/gate that opens the way for your card to being processed further.

Payment gateways are usually provided by a bank or mostly by PSP (payment service provider) — specialized financial institution.

As we know, one of the key differences of the online payments, is that we do not physically do any actions/manipulations with a card… we do not swipe it or put it on POS terminal, etc. which makes online transactions more vulnerable to fraud. And at this point payment gateway becomes a salvation tool as it takes the responsibility to check all the information a customer fills in, encrypt it and safely transfer it to the acquirer. As for the merchant, PG protects them from the fraud, inactive accounts, cards that are expired, or credit limits.

The next party who takes the action is called a Payment Processor.

Often we can see that these two terms (payment gateway and payment processor) are mistaken for each other or used as synonyms when in reality they are not the same.

As we mentioned before, after payment gateway completes verifying card details, he transfers payment request exactly to the payment processor.

Payment processor after receiving payment request sends the inquiry to the card association to transfer the funds from account to account. In turn, card association routes the transaction request to the card issuing bank to allow the payment. After these steps are done, the issuing bank either approves or declines the transactions and all thess steps move backwards and customer sees successful or failed transaction. At this point, some of you may wonder:

If the payment processor does all the functions mentioned above, what are the Payment Service Provider (a.k.a PSP) and Payment Facilitator are?

PSP is another term to call the payment processor and payment facilitator — it is all about the same.

Merchant accounts

Now you probably wondering how is it all connected to Merchant Accounts?

The answer is very simple. If you are an entrepreneur and want to receive/collect money/payments on your website, first off all, you’ll need a merchant account. Without the MID you could not operate as an entrepreneur and accept payments, especially not to your personal card from your website store, etc.

We should clarify what acquiring bank is. An Acquiring Bank (the merchant’s bank) is a financial institution that initializes and maintains contractual agreements with merchants for accepting and processing credit card transactions.

Whether you open a merchant account by yourself or through the third party, there are a lot of questions to be prepared for.

Read here↗︎︎ on how to open a merchant account.

The right start for every merchant is opening the right merchant account, choosing the right PSP, as it will definitely impact transactions’ acceptance ratio, chargebacks, fraud prevention and much more.

Genome is all-in-one new generation financial ecosystem aimed to help merchants* to keep and maintain all of their business and personal funds in one dashboard without crossing/mixing them. Genome enables merchants to open multiple MID’s, receive payments in 180 currencies, exchange them without fees. Zero risk for you and your customers with built-in anti-fraud tools.

*Please note that Genome’s merchant services have been temporarily unavailable since September 2024.