The payments world is shifting rapidly, and one of the most significant changes is the shift toward open banking. How does it differ compared to traditional banking methods? Open banking refers to the practice of allowing your bank to securely share your financial information or make payments with other authorized financial service providers.

If put simply, open banking occurs when third-party apps can directly interact with your bank accounts, rather than you having to log into each bank individually, which is essentially why it is called open.

At Genome, we adopted open banking tools to respond to strong demand for faster settlements and lower costs for our merchants.

In this guide, we will explain what an open banking system really is, how financial institutions enable it, and all about open banking integration.

What are open banking transactions?

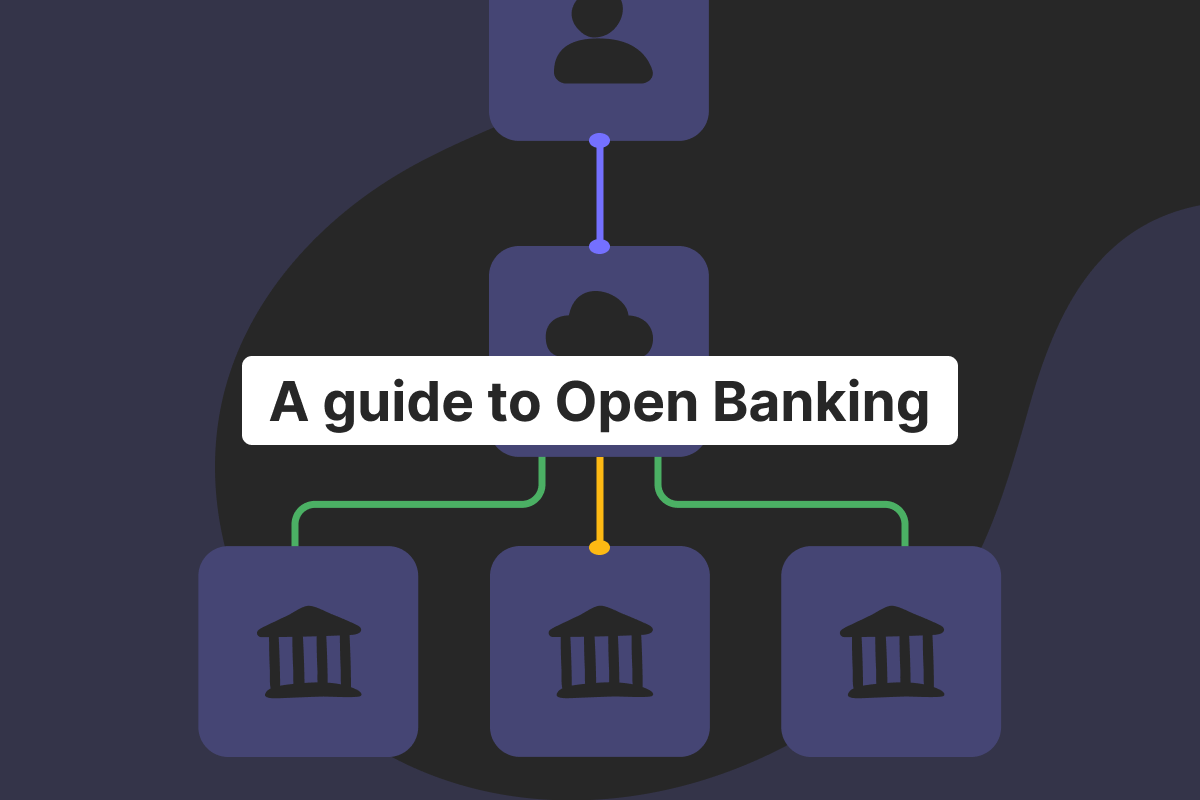

At its core, open banking technology is about securely sharing financial data between regulated financial institutions and authorized third-party providers through standardized open banking APIs. It provides an opportunity for customers and merchants to interact using direct bank payments.

Here are the key ideas:

Customer consent. It is a core pillar; only after that can the specific consumer data be shared or payment functions be executed.

Safe access. Only authorized payment providers or third-party service providers are permitted to connect.

Account-to-Account. Payments and fin-information flow directly between the user’s account and the merchant.

It is a big difference compared to a card network, where providers act as intermediaries. Besides this, there are other differences between open banking and traditional banking transfers:

Speed. Funds move much faster.

Cost. No card scheme fees.

Transparency. Merchants gain access to real-time transaction data.

Businesses in e-commerce, insurance, accounting, and, in general, the financial industry that adopt open banking can expect lower costs and better customer satisfaction due to faster payments.

How do open banking transactions work?

Open banking payment works pretty straightforward:

A customer selects open banking at checkout. Instead of providing card details, they opt for a direct payment option.

The financial provider connects securely to the user’s bank account. The regulated financial service provider, such as Genome, is utilizing open banking APIs to connect with the customer’s financial institution.

Strong Customer Authentication (SCA). One of the most important parts is that the customer confirms through biometrics or their banking app, protecting their data.

Funds move directly. Money is transferred from the user’s bank account to another account, with a full payment history stored for reporting purposes.

The idea of account-to-account payments isn’t new, but the automated process that can handle multiple transactions is a significant development. Behind the scenes, this relies on other payment service providers and fintech companies cooperating under PSD2 open banking regulations.

In other words, European regulation demands that fintech companies, third-party service providers, or any player on the market implement multifactor authentication. The reasoning behind this is that financial institutions can prevent data breaches or even the simple leaking of any customer’s financial data when using financial products.

For Genome’s merchants specifically, the result is near-instant (if SEPA Instant is used), reliable transactions with enhanced risk management, which is discussed in more detail below.

Open an account

in Genome online

Benefits of open banking for merchants

For merchants, the benefits of open banking go beyond lower fees:

Faster settlements. Near-instant payouts using SEPA Instant Transfers compared to multi-day card or SWIFT timelines.

Enhanced security. Encrypted APIs protect customer data and consumer data, ensuring secure access.

No chargebacks. Because these payments bypass card networks, which define the rules for chargebacks, the mechanism for reversing a payment simply does not exist. Note: consumers may still dispute payments under consumer protection laws/request refunds through their bank

Better reporting. Merchants access real-time financial data and detailed transaction information.

Higher client satisfaction. A smoother process reduces checkout abandonment.

If we are more specific, consider, for example, e-commerce. The benefits of open banking for merchants directly tied to an alternative payment method, known as Pay-by-bank, are particularly relevant. By utilizing open banking features, merchants can accept payments directly from a customer’s bank account, enjoying all the benefits listed above.

Despite its relatively new introduction to the industry, Pay-by-bank is showing significant growth in adoption and transaction volume, particularly in the UK and certain EU countries. Pay-by-bank is now among some of the most popular payment methods in the financial sector in the UK, Netherlands, Finland, Spain, and Germany, with one-third of those aged 18-29 using it either daily or weekly, according to research.

At Genome, we strengthen these advantages with compliance and adherence to major security regulations, built-in fraud prevention, and our own advanced anti-fraud tools – key in today’s financial sector.

Genome merchant accounts and open banking

With our merchant services currently in BETA testing, Genome provides more than a simple merchant account. It’s our little hub for innovative financial services designed for modern commerce. With Genome, merchants get:

Access to open banking. Merchants can receive SEPA Instant and Credit Transfers from customers across Europe! Securely and within seconds if the SEPA INST is used.

Multi-currency support. Our clients get access to multi-currency accounts in USD, GBP, EUR, PLN, CHF, JPY, CAD, CZK, HUF, SEK, AUD, and DKK, allowing them to store and send SWIFT payments with transparent currency exchange. Moreover, you can issue virtual and physical Visa debit cards and link them to most of these currencies!

Fraud prevention. Up-to-date security tools for the safety of customer financial data.

Analytics. Access to transaction history and financial information in one place.

Integration flexibility. Use customizable hosted payment pages for checkout and better financial management.

Multiple banks. Genome connects to other financial institutions across Europe, streamlining the acceptance process.

Genome makes open banking features accessible to even smaller businesses that once relied solely on cards. But if you require more for general business finance services, consider opening a dedicated business account – you can upgrade to a merchant one easily! It would be a huge upgrade for payment processing.

Open an account

in Genome online

Open banking vs. traditional payment methods

For years, digital payments have relied on card networks and wire transfers. They became the backbone of online transactions, but also carried the baggage of the past.

Credit and debit cards, for example, still dominate e-commerce, yet they come with processing fees that eat into margins, delays before funds actually reach a merchant’s account, and the constant risk of chargebacks.

On the other side, SEPA and SWIFT transfers are trusted for their security, but they are often expensive — particularly when international intermediaries are involved.

Open banking takes a different path. Instead of layering payment networks on top of each other, it creates a direct link between the customer’s account and the merchant.

No middlemen, no multi-day waiting periods, no uncertainty over hidden fees. Transactions are confirmed in real time, with the consumer authorizing payment through their familiar banking app. What once required several steps and multiple players is reduced to a single, transparent interaction.

The result is not just another payment option, but a fundamental upgrade. We treat open banking as a future-ready alternative to traditional methods in the banking industry.

Business use cases for open banking

Open banking fits a wide variety of industries in the banking services ecosystem:

E-commerce stores. Direct bank payments improve conversions.

Subscription-based services. Reliable recurring billing without card expiry issues.

Marketplaces. Faster settlements across multiple financial institutions, boosting trust.

B2B invoice payments. Streamlined and, most importantly, uninterrupted payments make cash flow management easier.

Account aggregation. Merchants can offer value-added financial products by connecting multiple accounts for customers.

Personal finance apps. The embodiment of the open banking concept, by linking financial accounts from other financial institutions to a third-party provider, apps can offer account aggregation, budget management, and access to financial products such as loans or savings accounts.

Insurance providers. With instant verification of financial data and real-time transaction data, insurers can automate collection and claims payouts, reduce the risk of data leaks, and make financial services better.

Together, these examples show that open banking services are not limited to a single niche of the financial services industry. From retail to B2B, from financial institutions to third-party providers, the ability to access and process customer data and banking data through open banking APIs (application programming interfaces) creates a more connected financial sector.

The practical outcome is faster operations, lower costs, improved financial services and payment services, and entirely new ways to build trust with customers.

How to enable open banking with Genome

First of all, we highly recommend checking our merchant account page. You may find all the information you potentially need when looking for merchant financial services.

Enabling open banking is simple:

Sign up for a Genome business wallet.

Onboarding. Provide company details to Genome’s compliance team.

Once you have a business wallet, you can apply for a merchant account. Or multiple merchant accounts, if you need them.

Integration. Follow our instructions for merchant services integration.

And that’s it! Now you can collect funds, receive notifications for incoming customer payments via API, monitor real-time financial data, and perform payouts using SEPA Credit and Instant Transfers.

Future of open banking

The future looks bright for open banking initiatives and services, and companies in the financial industry are even more optimistic than they were at the time of the early PSD2 regulation rollout.

The reason for that is the expansion of PSD3. Upcoming open banking regulations are expected to strengthen both consumer rights and security standards.

Why is it important? In short, PSD2 made open banking possible; PSD3 will make open banking scalable for financial institutions.

Stricter compliance will ensure that banking data, consumer data, and customer data remain fully protected, while secure access protocols will be improved. It is especially important as financial institutions cooperate with third-party solutions and payment service providers across borders.

The final text for the Third Payment Services Directive (PSD3) is still under discussion by the European Parliament and Council and is expected to be adopted in 2025; however, it is more likely to come into effect between late 2026 and early 2027.

Not only Europe. Beyond the EU, regions such as the UK, Asia, and North America are developing their own payment services frameworks. It means that more financial institutions will begin offering standardized connections, making financial transactions smoother for merchants and safer for clients’ financial data worldwide. Businesses with multiple banks will benefit from consolidated oversight and faster settlement processes.

Integration across financial services. Open banking is not only about faster bank payments – it’s also about transforming the financial services industry. Expect wider access to accounts, digital wallets, and bundled financial products. Additionally, account aggregation will enable consumers and businesses to view all their financial accounts in a single dashboard, complete with detailed transaction data and transaction history.

The integration creates an opportunity for ultimate financial services that combine payments, lending, and even investment options without any threat to customers’ financial data.

Fintech will continue to grow, and businesses will reap the benefits. As regulation matures, fintech companies will play a bigger role in building tools for other financial service providers and merchants. From enhanced fraud prevention solutions to predictive analytics based on financial data, the ecosystem will expand.

Importantly, these solutions will enhance customer satisfaction by reducing fraud, preventing financial data leaks, and ensuring transparency, ultimately leading to increased customer retention.

In summary, the future of open banking technology will rely on a level of collaboration between businesses and financial institutions that has never been seen before.

Open an account

in Genome online

FAQ

Are open banking transactions safe?

Yes. Regulated financial institutions, strong anti-fraud measures, and encrypted banking data ensure maximum security.

How fast are open banking payments?

Most are near-instant, unlike traditional banks or card systems.

Can I accept open banking payments without a merchant account?

No. You need a regulated bank or electronic money institution, such as Genome, to handle them.