SEPA Transfers

Business services

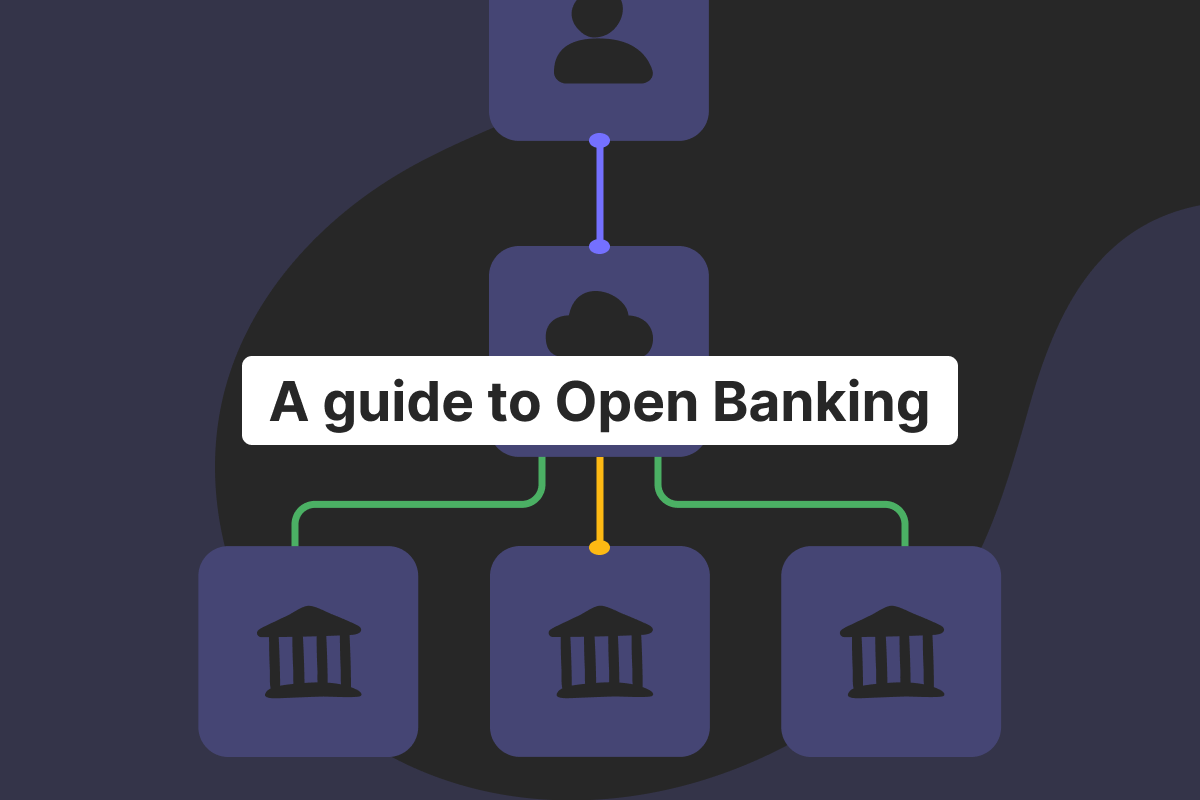

What is an Open Banking payment? Benefits and use cases

An Open Banking payment is a direct bank-to-bank transfer initiated at checkout, where the customer approves the payment inside their own banking app. Instead of entering card details, the buyer is securely redirected to their bank, confirms the amount, and the transfer is sent straight to the merchant. It became popular as more financial institutions started sharing customer-permitted financial data through regulated frameworks. With Open Banking APIs, licensed third-party providers can connect to banks to start payments and confirm them, without exposing sensitive credentials. Key benefits include strong authentication, fewer fraud vectors, and faster confirmation. It can also simplify reconciliation,

Money and you

SEPA vs. SWIFT transfers: key differences explained

SEPA (Single Euro Payments Area) is a European payment scheme that enables euro transactions across participating countries, making domestic-style transfers possible across borders. It’s designed for payments in EUR between bank accounts held at a bank in the SEPA zone. It has rules around formats, timelines, and fees, especially for SEPA payments. SWIFT (Society for Worldwide Interbank Financial Telecommunications), by contrast, is a global messaging network used by financial institutions to route payment instructions worldwide. It’s often associated with cross-border wires and correspondent chains, which is why swift payments can involve more intermediaries, variable fees, and less predictable settlement speed.

Business services

What is an instant bank payment? A complete guide for businesses

Do you like the idea of instant transactions, instant payments? If you’ve ever waited a day (or two) for a bank transfer to land, you already know why instant bank payments became such a big deal. Nobody wants to wait to transfer money or listen to “tomorrow morning” or “during regular business hours.” This is where instant bank payments come in. They allow money to move between bank accounts in seconds, giving companies and consumers a faster, safer, and cheaper way to get paid. If the instant payment system is such a big deal, why do many still choose to

Business services

What are dedicated IBANs for businesses? A guide

A dedicated business IBAN is now a key element in the global digital economy. Modern business processes need to combine clarity with easy payment reconciliation and compliance. For this reason, a dedicated IBAN account offers a convenient way to send money and receive incoming payments seamlessly. Genome is a regulated European Electronic Money Institution (EMI) that provides business accounts for businesses looking for simpler payments. Whether you carry out international trade or need to pay suppliers abroad, the right IBAN accounts will help your business. What is a dedicated IBAN? An IBAN is an International Bank Account Number. It’s used

Product news

Introducing the Verification of Payee (VOP): no more misdirected SEPA Transfers!

At Genome, we are always on top of your security, implementing the necessary features to keep your money and data protected, as well as safeguarding transactions from errors. The Verification of Payee service is perfect for the latter! As of next week, we are implementing a Verification of Payee, a huge security and quality-of-life feature. It will apply to SEPA Transfers within Genome, for both personal and business wallet users. Verification of Payee (or in short, VoP) is a security measure in the SEPA payment system designed to combat fraud and misdirected payments. It verifies that the name of the

Money and you

What are Faster Payments? A complete guide

The Faster Payments system (sometimes referred to as FPS) is not just a regular payment system, but one of the few UK interbank payment systems that enables payers to make instant payments. Instead of waiting days for transfers, users can send funds instantly, and FPS will process payments the same day. In this guide, we’ll explain what Faster Payments really are, how they work, and how they compare to other systems. What is the Faster Payments Service (FPS)? The Faster Payments service is a United Kingdom-based payment system introduced by the UK Payments Council (now Pay.UK) in 2008. From the

Business services

Local IBANs explained: what are they and why businesses need them

Local IBANs help your business get paid like a local, even when you operate across borders. Instead of relying on one universal account setup, you receive a country-specific account number that customers recognize and trust. For many buyers, paying into a domestic bank account feels faster and more familiar than sending money abroad. This matters when you work with partners, marketplaces, or clients who want simple checkout and clear payment details. Local IBANs also make international payments easier to track and reconcile, because transfers follow standard banking formats used by financial institutions. In short, they reduce friction in cross-border payments

Money and you

Difference between CHAPS and Faster Payments

When looking at CHAPs and the Faster Payments service, it pays to make the right decision. Cost is one of the key factors when choosing between these two methods of sending money to a recipient’s bank account. Business efficiency is another point to take into account when looking at recurring bank transfers or one-off payments. To make the right decision, we need to look in depth at these payment types and how they work. What is CHAPS? The question of what a CHAPS payment is is easy to answer. It is the Clearing House Automated Payment System, used for same-day,

Business services

What is a money transfer API? A complete guide

We aim to explain what APIs (application programming interfaces) truly represent and how financial institutions utilize API banking to facilitate money transfers. The reason for that is twofold: first, the growing popularity of using API to send money or utilize other financial services, and second, Genome, as a provider of API-driven payment tools, sometimes faces questions from clients such as “What is banking API,” “Do I need API for a bank account,” and so on. Discover what API banking is and how Genome utilizes APIs for its financial services below. What is an API money transfer? In broad terms, a