An Open Banking payment is a direct bank-to-bank transfer initiated at checkout, where the customer approves the payment inside their own banking app. Instead of entering card details, the buyer is securely redirected to their bank, confirms the amount, and the transfer is sent straight to the merchant.

It became popular as more financial institutions started sharing customer-permitted financial data through regulated frameworks. With Open Banking APIs, licensed third-party providers can connect to banks to start payments and confirm them, without exposing sensitive credentials.

Key benefits include strong authentication, fewer fraud vectors, and faster confirmation. It can also simplify reconciliation, because payments carry clear reference details.

Common use cases:

E-commerce checkouts, especially for higher-value orders.

Subscription renewals, where customers prefer bank authorization.

Marketplaces that need reliable, traceable incoming payments.

Digital merchants offering modern financial services across regions.

Looking ahead, open finance expands the model beyond payments, using permitted financial data across more products and providers. All supported by financial institutions working within secure standards.

Open an account

in Genome online

What is an Open Banking payment?

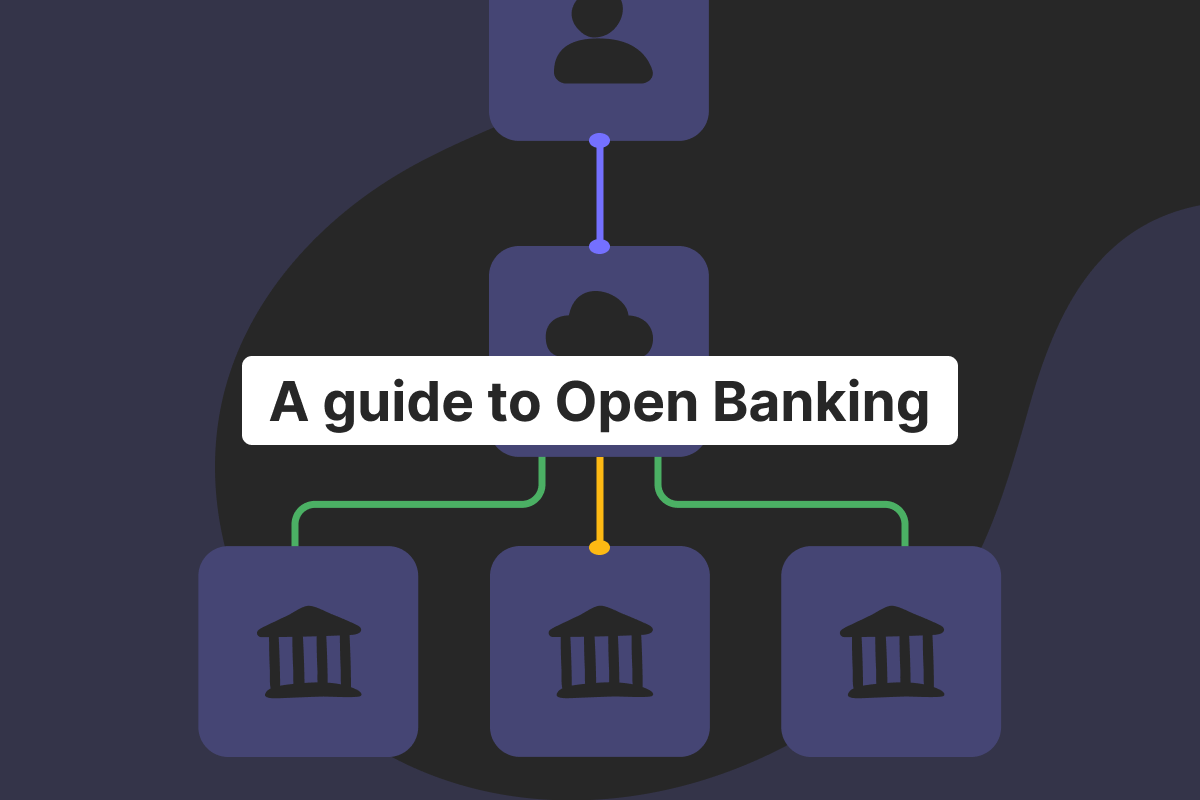

An Open Banking payment is a simple way to pay online straight from your bank account, without using a card. Instead of typing in card details, the payment is started through Open Banking connections (often called Open Banking APIs) and then approved inside your own banking app.

Here’s how it works in practice. At checkout, the merchant offers Open Banking services as a payment option. When you choose it, the payment request is sent to your bank. You’re redirected to your banking app, where you review the amount and authorize the transfer. This approval step is protected with SCA (Strong Customer Authentication), which usually means something you know (like a passcode) plus something you have or are (like a phone confirmation or biometrics). Once you confirm, funds move directly from your account to the merchant’s account as an account-to-account (A2A) transfer.

Because the money goes from bank to bank, there are no card numbers involved, and there’s less reliance on extra intermediaries. That can mean fewer fraud risks and, in many cases, lower processing costs for merchants.

This model grew fast in Europe thanks to the Payment Services Directive, which pushed financial institutions to enable secure access and standardize how consent works. In this setup, banks can share permitted financial data and customer financial data only with regulated parties, like payment initiators and other financial service providers, and only when the customer agrees.

Benefits and use cases are easy to see: smoother e-commerce checkout, instant confirmation where supported, and better traceability for subscriptions and invoices. It also opens the door to more innovative financial services built on real-time permissions and clearer account information, which is something many traditional banks now support through broader Open Banking initiatives.

As more financial institutions adopt these standards, Open Banking payments are becoming a practical, secure option within modern financial services.

How Open Banking payments work

Step 1: A customer chooses “Pay by Bank” at checkout instead of a card.

Step 2: The customer is redirected to their bank app via API. On the technical level, the checkout connects to the customer’s banking app using Open Banking APIs and secure access controls.

Step 3: The customer authenticates and confirms the payment using Strong Customer Authentication, so the bank can verify identity and intent.

Step 4: Funds transfer instantly through the bank system. The money moves account-to-account between bank accounts. In the EU, it would often be via SEPA.

Step 5: The merchant receives confirmation. The merchant gets a fast status update, which helps fulfillment and reconciliation.

Behind the scenes, Open Banking relies on permissioned connections between financial institutions and regulated financial service providers.

Put simply, Open Banking enables pre-approved financial transactions between banks and financial providers, which is why it is so fast.

It means an Open Banking checkout can start from a customer’s bank account and move funds without sharing card credentials, because the client already shared his own data with the bank.

It enables fast banking transactions and secure data sharing with other financial institutions, because consumer data can be visible only by Open Banking market participants.

Open Banking payments vs card payments

Feature | Open Banking | Card payment |

Fees | Often lower (no card network fees) | Higher due to scheme fees and processing |

Settlement | Real-time or near real-time (for example, SEPA Instant usually takes 10 seconds) | Typically 1–3+ days depending on clearing |

Chargebacks | Usually no chargebacks on bank transfers | Chargebacks are common and costly |

Fraud | Lower for many flows (bank-level SCA) | Higher exposure to card fraud vectors |

Data entry | No card number entry | Card number, expiry, CVV often required |

Ideal for | Subscriptions, high-ticket, EU cross-border using euro | Broad acceptance, global cards |

Benefits of Open Banking payments for businesses

Open Banking solutions are not magic pills, but innovative services. These are the benefits:

Lower processing costs (especially compared to traditional card fees): traditional payment methods are heavily dependent on third-party payment processors. It is simple – no middleman, no fees.

Instant settlement for improved cash flow (where instant payments are supported): the best part, there are not multiple but many financial institutions (thousands across the European Union only) which are a part of an Open Banking framework.

Higher security via bank-level authentication and SCA: data access for an outsider is impossible.

Reduced fraud and typically no chargebacks: account-to-account exchange data makes fraud less of a problem (phishing websites have no chance to authorize in the Open Banking).

Higher acceptance and fewer failed payments (no expired cards): it’s more about friendly account management for customers, but it boosts statistics.

Better checkout conversion (no card details to type): you are not touching banking data nor customer data either. No data protection needed – no security risks.

Perfect for subscriptions & high-ticket items: because it is.

Open Banking payments in Europe

At some point, Open Banking financial services were a popular choice. Now, due to the EU Payment Services Directive, it is the law.

These Open Banking regulations encouraged banks and other financial institutions to support safe access to account information, Open Banking apps, payment services, and payment initiation.

Major financial institutions are also required to provide secure APIs for regulated access.

As a result, many financial institutions and other regulated financial service providers now provide APIs that allow regulated partners to connect for payments and, when permitted, financial data access.

In this model, third-party providers can initiate payment services with the customer’s consent, while keeping sensitive information protected. They also set expectations for how customer data and permitted financial data can be shared safely. Real-time settlement often happens through SEPA rails, with Open Banking payments frequently paired with SEPA Instant Transfers for faster clearing across the region. Check Genome’s services to see for yourself!

Open an account

in Genome online

Open Banking payments vs instant bank payments

These two concepts work together, inside Genome, but they’re not the same thing. Open Banking is the method or interface: it connects checkout to multiple banks through secure connections, so the customer can approve a payment inside their Open Banking apps. That approval step is what makes Open Banking services feel smooth and familiar for business customers and their buyers.

Instant bank payments are the rails: they’re the payment network that actually moves money quickly (for example, SEPA Instant in the EU). In practice, Open Banking starts and verifies the payment request, while the instant payment capabilities help deliver the funds fast.

So, think of it like this: Open Banking handles initiation and authentication, and instant bank payments handle the speed of settlement. Used together, they create faster, simpler financial services that move money straight from a bank account to the merchant.

Use cases for Open Banking payments

E-commerce & online retail

Open Banking payments make checkout quicker because customers approve the transfer in their bank app, with fewer steps than cards.

SaaS & subscription billing

For recurring charges, the Open Banking system helps reduce failed renewals caused by expired cards and supports clearer payment references.

Marketplaces (seller payouts)

Marketplaces can collect funds and manage seller payouts more smoothly, especially when payments touch different providers and reporting needs.

Travel, insurance, telecom

These sectors benefit from fast confirmations for high-value purchases, bill payments, and time-sensitive services, often supported by modern financial technology.

Crypto exchanges & fintech

For regulated platforms, bank-authorized transfers can improve traceability and reduce chargeback exposure in parts of the financial industry.

As Open Banking initiatives continue, more financial products are being built on secure data permissions, moving the market toward open finance, where sharing and using financial access is broader across services and providers.

How Genome supports Open Banking payments

Genome helps businesses accept Pay by Bank payments by combining accounts, settlement, and checkout tools in one setup for the financial services industry. All is done via our instant bank payments feature. You can open business accounts with dedicated IBANs, so incoming payments are easy to route and reconcile. For faster settlement in the EU, Genome supports SEPA Instant, where available, helping merchants receive funds quickly after customer approval.

To power Open Banking connectivity, Genome enables Pay by Bank functions that let customers authorize payments securely through their own bank.

Clients can also manage multi-currency accounts for cross-border operations, keeping instant payouts organized in one place.

Unlock corporate virtual cards for seamless subscription and online payments management, or order corporate physical cards for in-person payments.

For merchant operations, Genome provides tools like hosted payment pages and merchant account instruments for better management. Add fast, digital onboarding, and you get a practical way to launch and scale financial products inside a connected financial ecosystem.